What is the GNSS Chip Market Overview – definition, scope, and significance?

The GNSS (Global Navigation Satellite System) chip market comprises semiconductor devices that receive signals from satellite constellations such as GPS, GLONASS, Galileo, and BeiDou. These chips enable precise positioning, navigation, and timing functionalities across a broad array of electronic products. The market’s scope extends from consumer gadgets to aerospace, automotive, and defense platforms, making it a critical enabler for emerging IoT, autonomous vehicles, and location‑based services. Its significance lies in driving connectivity, safety, and operational efficiency in modern digital ecosystems.

What are the GNSS Chip Market drivers, restraints, challenges, and opportunities?

Key drivers include the proliferation of smartphones, expanding automotive telematics, and escalating demand for high‑accuracy location services in logistics and surveying. Restraints involve high R&D costs, stringent regulatory compliance for defense applications, and supply‑chain risks for advanced semiconductor materials. Challenges stem from intense competition and the need for low‑power, multi‑constellation solutions. Opportunities arise from 5G integration, growth of autonomous navigation, and the rollout of new satellite constellations that enhance coverage and reliability.

What are the current GNSS Chip Market growth trends?

Current trends highlight a shift toward multi‑band, multi‑constellation chips that deliver centimeter‑level accuracy while conserving power. Integration of GNSS functionality with cellular and Wi‑Fi modules is becoming mainstream, especially in smartphones and in‑vehicle infotainment systems. Additionally, the emergence of chipsets optimized for edge AI enables real‑time processing of positioning data, supporting advanced mapping, augmented reality, and precision agriculture applications.

How did COVID‑19 impact the GNSS Chip Market and what is the recovery trajectory?

The pandemic initially suppressed demand due to factory shutdowns and reduced consumer spending on premium devices. However, remote work and increased reliance on location‑based services accelerated demand for navigation and timing solutions in logistics and telehealth. By late 2021, production normalized and the market entered a recovery phase, benefiting from pent‑up demand for new smartphone launches and a rebound in automotive manufacturing, setting the stage for sustained growth.

What does the GNSS Chip Market competitive landscape look like?

The competitive landscape is characterized by a mix of large semiconductor giants and specialized navigation firms. Companies such as Broadcom, Qualcomm, and MediaTek leverage extensive design ecosystems, while u‑blox, Septentrio, and Trimble focus on high‑precision, niche applications. Recent consolidation activity includes strategic acquisitions to broaden portfolio breadth and geographic reach, intensifying rivalry in both consumer and industrial segments.

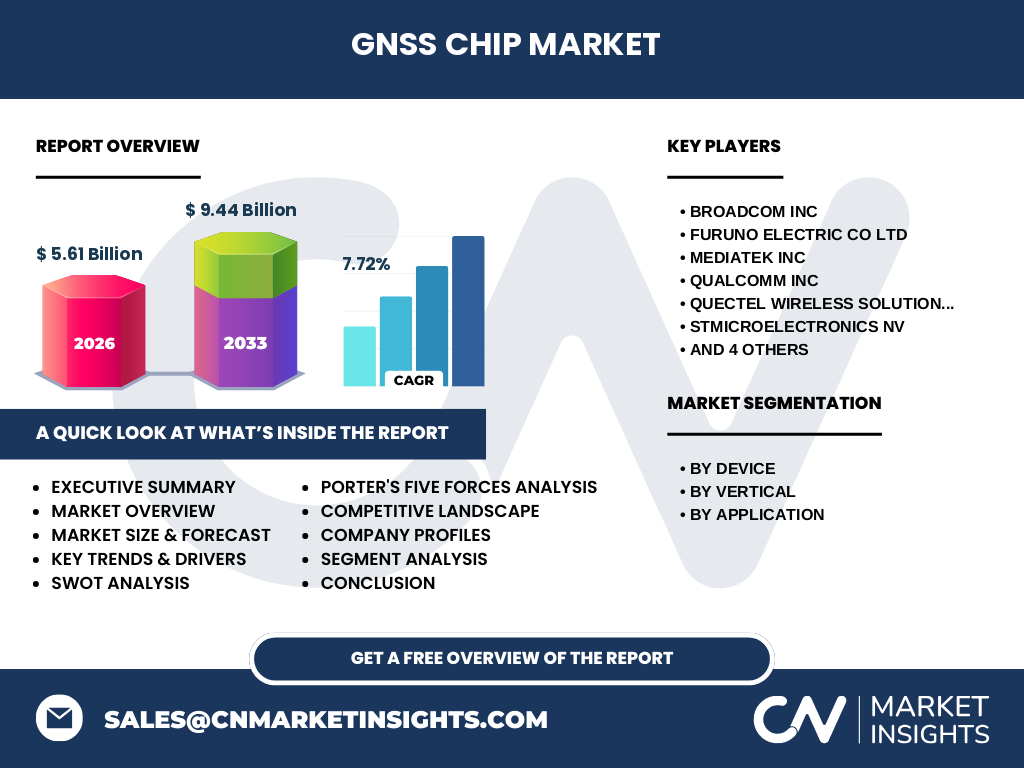

What are the key findings in the Executive Summary of the GNSS Chip Market?

The GNSS chip market is valued at USD 5.61 billion in 2026 and is projected to reach USD 9.44 billion by 2033, reflecting a CAGR of 7.72 % over the forecast horizon. Growth is propelled by expanding smartphone penetration, automotive connectivity, and the rise of location‑centric services across verticals. Multi‑constellation, low‑power designs are reshaping product roadmaps, while competitive pressures drive continuous innovation and strategic partnerships.

What is the GNSS Chip Market forecast for 2025‑2032?

Building on the disclosed CAGR of 7.72 %, the market is expected to maintain steady expansion through 2032, surpassing the USD 9 billion threshold by the early 2030s. The forecast anticipates incremental gains each year, driven by higher adoption rates in automotive telematics, increased shipments of GNSS‑enabled consumer electronics, and expanding use cases in industrial IoT and defense sectors.

How is the GNSS Chip Market size and share segmented by device, vertical, and application?

By device, the market is split among smartphones, tablets, personal navigation devices, and in‑vehicle systems, with smartphones holding the largest share due to ubiquitous integration. Vertically, consumer electronics dominate, followed by automotive and transportation, military and defense, and marine segments. Application‑wise, navigation and location‑based services lead, while mapping & surveying, telematics, and timing & synchronization each represent significant, growing niches.

What is the global GNSS Chip Market size and share by region?

The market’s global footprint reflects strong demand across North America, Europe, Asia‑Pacific, and Rest of World. While exact regional monetary values are not disclosed, Asia‑Pacific contributes the highest share owing to robust smartphone manufacturing, rapid automotive electrification, and extensive IoT deployments. North America and Europe follow, driven by advanced automotive safety standards and defense spending.

What are the detailed regional analyses of the GNSS Chip Market?

In Asia‑Pacific, China, Japan, and South Korea lead chip integration in consumer devices and vehicle platforms, supported by aggressive 5G rollouts. North America shows strong growth in autonomous vehicle pilots and defense contracts, with the United States as a major consumer of high‑precision GNSS solutions. Europe focuses on regulatory‑driven adoption in automotive safety and railway signaling, while emerging markets in Latin America and the Middle East exhibit rising demand for navigation in logistics and marine applications.

Which leading companies operate in the GNSS Chip Market and what are their strategies?

Key players include Broadcom Inc, Furuno Electric Co Ltd, MediaTek Inc, Qualcomm Inc, Quectel Wireless Solutions Co Ltd, STMicroelectronics NV, Septentrio NV, Skyworks Solutions Inc, Trimble Inc, and u‑blox Holding AG. Strategies range from expanding multi‑constellation portfolios, investing in low‑power fabrication processes, forging partnerships with automotive OEMs, to acquiring niche firms that enhance precision‑positioning capabilities. Many are also pursuing joint development with satellite operators to optimise chip performance.

How does Porter’s Five Forces analysis apply to the GNSS Chip Market?

Threat of new entrants is moderate due to high entry barriers such as advanced semiconductor fabrication and extensive IP. Bargaining power of suppliers is relatively strong because of limited sources for specialized silicon wafers and RF components. Bargaining power of buyers is growing as large OEMs demand cost‑effective, integrated solutions. Threat of substitutes is low; alternative positioning technologies (e.g., BLE, Wi‑Fi) complement rather than replace GNSS. Competitive rivalry is intense, driven by rapid innovation cycles and price competition.

What are the SWOT insights for the GNSS Chip Market?

Strengths: Proven technology, universal applicability, and increasing demand for precision. Weaknesses: High development costs and dependence on satellite infrastructure. Opportunities: Expansion into autonomous systems, 5G‑assisted positioning, and new satellite constellations. Threats: Geopolitical restrictions on satellite access and potential supply‑chain disruptions for advanced semiconductor materials.

What does the GNSS Chip Market value chain look like?

The value chain starts with raw material suppliers (silicon, RF components), proceeds to design houses that create IP cores and reference designs, followed by semiconductor fabs that manufacture the chips. Next are test and packaging facilities, then original equipment manufacturers (OEMs) that integrate chips into devices. Finally, distributors and end‑users (consumers, automotive makers, defense agencies) complete the chain, with after‑market support and firmware updates playing a crucial role.

What key investment insights can be drawn from the GNSS Chip Market?

Investors should target companies with diversified multi‑constellation portfolios and strong automotive alliances, as these segments promise higher margins. Early‑stage players focusing on ultra‑low‑power, edge‑AI enabled chips offer high growth potential. Monitoring satellite‑operator partnerships can also reveal winners, while supply‑chain resilience and IP strength remain critical risk mitigators.

What is the final conclusion of the GNSS Chip Market analysis?

The GNSS chip market is on a robust growth trajectory, underpinned by ubiquitous demand for precise location services across consumer, automotive, and defense domains. With a projected CAGR of 7.72 % and a market size surpassing USD 9 billion by the early 2030s, the sector offers ample opportunities for innovation, strategic partnerships, and attractive returns for forward‑looking investors.

How was the research methodology designed for this GNSS Chip Market report?

The study combined primary interviews with industry executives, secondary data from reputable databases, and quantitative modelling using the provided market size and CAGR. Trend analysis, competitive benchmarking, and scenario planning were applied to generate forecasts and strategic insights. Validation steps included cross‑checking with supplier shipments and public financial disclosures of key players.

What is the scope of the GNSS Chip Market research?

The scope covers GNSS chips used in smartphones, tablets, personal navigation devices, and in‑vehicle systems, across consumer electronics, automotive, military, and marine verticals. Applications examined include navigation and location‑based services, mapping and surveying, telematics, and timing & synchronization. Geographically, the research spans North America, Europe, Asia‑Pacific, and Rest of World, capturing both mature and emerging markets.

Which key companies and recent developments are shaping the GNSS Chip Market?

Broadcom announced a new multi‑constellation RF front‑end that improves power efficiency for 5G smartphones. Qualcomm unveiled a chipset integrating GNSS with its Snapdragon platform, targeting automotive ADAS. u‑blox released a high‑precision timing module for industrial IoT. Trimble introduced a survey‑grade GNSS receiver with AI‑based error correction. MediaTek expanded its GNSS portfolio to support emerging satellite networks, while STMicroelectronics launched a low‑power GNSS solution for wearables.